The Pattison Crash: Robert and Walter Pattison and the 1898 Blending Bubble That Nearly Killed Scotch

In 1898, in a tied public house somewhere in Britain, an African grey parrot on a perch behind the bar said, to no one in particular, “Buy Pattisons’ whisky.” It had been trained to. There were, by the firm’s own account, around five hundred of these birds, distributed free to publicans across the country by a blending house in Leith, each one a small feathered billboard repeating the brand name at drinkers who had come in for something else. It is the detail everyone remembers about the Pattisons, and I want to start with it because it is the most honest thing about them. A parrot does not know what it is saying. It has been given a phrase and a reason to repeat it, and it repeats it with total conviction and no underlying assets whatsoever. That is also, more or less, a complete description of the company that bought the birds.

Almost everyone this site writes about built something. The reason I am writing about Robert and Walter Pattison is that they are the rare pair that whisky history remembers for nearly destroying the thing. Their collapse in December 1898 is the single event that ended Scotch’s Victorian boom, and the structure of how they fell (over-leverage, inflated inventory, dividends paid out of borrowed money, a cascade that took down the firms wired to them) is so clean a specimen of systemic failure that you could teach it in a finance course or a systems-reliability seminar without changing a word. The bottle on my shelf is shaped, very faintly, by the fact that these two men existed.

Dairymen who found a faster commodity

The Pattisons did not come from whisky. The family business was an Edinburgh dairy (wholesale milk and provisions), and Robert and Walter took it over from their father in the ordinary way that sons take over a family firm. What they noticed, in the mid-1880s, was that the thing they were already good at, which was buying a commodity cheaply and moving it at volume, applied even better to a commodity that did not spoil in a week and that the entire British middle class had suddenly decided it wanted.

The timing was not their insight; it was their luck, and I want to be fair about the difference. In the 1880s the brandy supply of Europe collapsed. The phylloxera aphid had been eating its way through French vineyards for two decades, and by the late 1880s Cognac, the after-dinner drink of the respectable classes, was scarce and dear. Blended Scotch whisky, made drinkable and consistent by the marriage of light grain spirit from the Coffey stills that John Haig and his peers ran at places like Cameronbridge with characterful malt from the Highlands, walked into the gap. Demand went vertical. Anyone with a warehouse, a recipe, and a salesman’s nerve could grow fast.

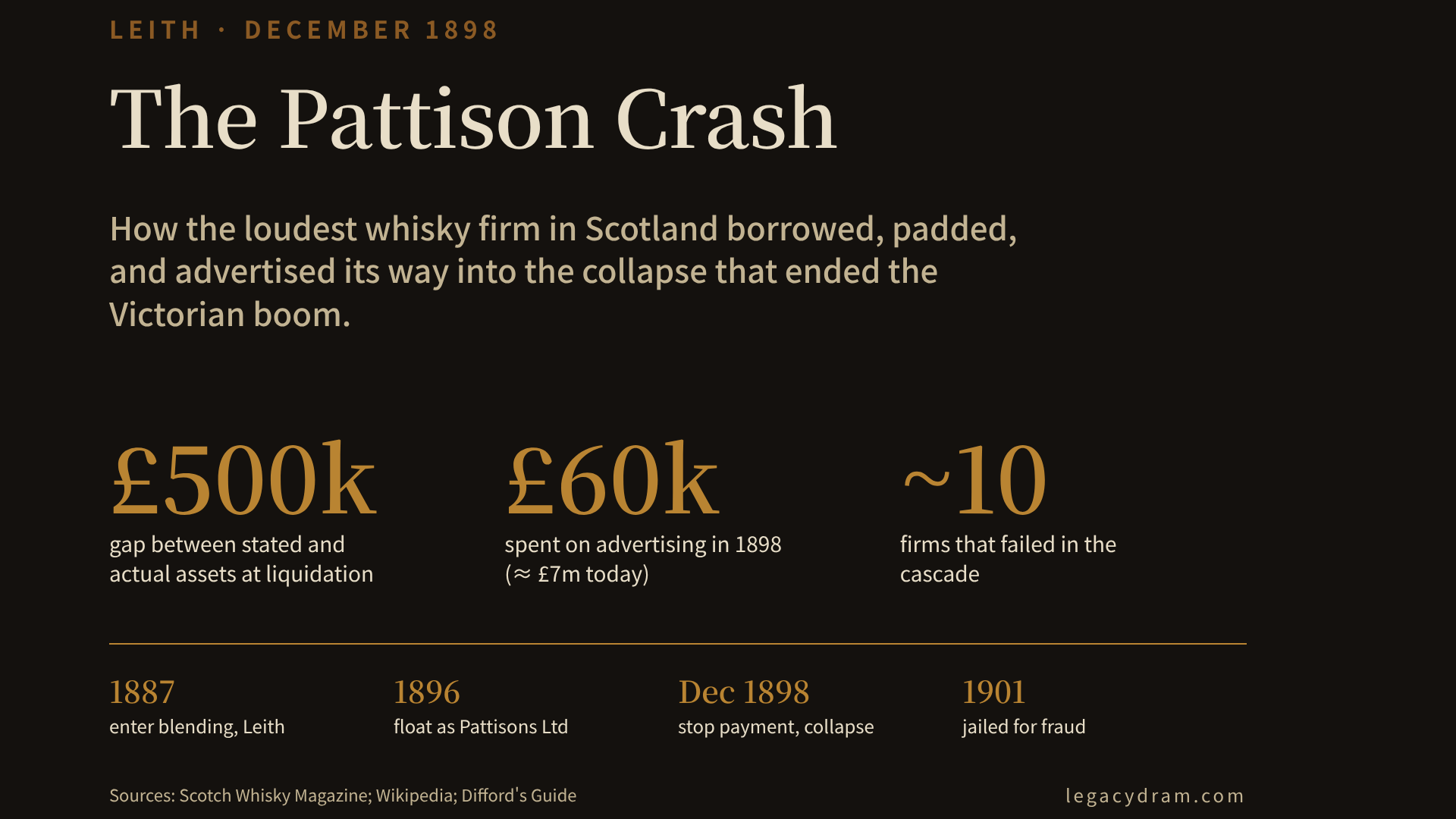

The Pattisons entered whisky blending around 1887, working out of offices on Constitution Street in Leith, the port district of Edinburgh, and they grew exactly as fast as the market allowed. By 1896 they had incorporated as Pattisons Ltd and floated a minority of the shares to the public, riding what turned out to be the very last and highest wave of Victorian whisky speculation. With the proceeds and with credit they bought their way upstream into production: a half-share in Glenfarclas, stakes in Aultmore and in Oban, the Ardgowan grain distillery, and, because why not, a brewery at Duddingston. On paper they had become a vertically integrated drinks company in under a decade. On paper.

What they chose, and what they padded

Here is where the engineering reading begins, because the Pattisons’ real product was not whisky. It was the appearance of a company that was worth more than it was, sustained long enough to borrow against the appearance.

They made three moves, and each one is a recognisable failure mode.

The first was leverage dressed as growth. The acquisitions upstream were largely financed by borrowing and by the float, and the firm serviced its obligations and kept its share price aloft by paying dividends, generous ones, out of operating capital rather than out of profit. This is the oldest unstable structure there is: a system that can only remain solvent as long as new money keeps arriving to pay the returns promised to the old money. It is a pyramid with a respectable address. It does not fail gradually. It runs perfectly until the inflow stutters, and then it fails all at once.

The second was inventory fraud, and this is the one that should make any engineer wince, because it is mark-to-myth accounting applied to a physical good. The Pattisons took cheap grain spirit, blended in a small quantity of genuine fine malt, and sold the result as “Fine Old Glenlivet,” at the time a quasi-generic prestige label that real Speyside whisky traded under. The receivers later found this single practice had inflated the firm’s stated profits by something close to £27,000. Restated in plain terms: they wrote up the value of their warehoused stock by relabelling it, and then borrowed against the written-up number. The casks in the warehouse were exactly as good as they had always been. The number attached to them was fiction.

The third was simply spending the difference loudly enough that no one looked. The advertising budget went from around £20,000 in 1897 to over £60,000 in 1898, or close to seven million pounds in today’s money, spent on print, on hoardings, and on the parrots. A firm spending at that rate in public does not look like a firm quietly running out of cash. That was the point.

I would like to tell you, at this stage, that the Pattisons were criminal geniuses operating an intricate machine. They were not. They were running a very ordinary machine (borrow, inflate the asset, pay the dividend out of the borrowing, advertise over the noise of it) louder than anyone else in the trade. The loudest seller is reliably the first one you hear going under.

December 1898

The inflow stuttered. In early December 1898 Pattisons Ltd stopped payment. On the fifth of the month the company’s preference shares (the supposedly safe, senior stock) fell by fifty-five percent in a matter of days. The Distillers Company Limited, the grain-whisky combine that everyone in the trade owed money to, froze the Pattison account over an unpaid balance of around £30,000; the banks declined to extend further credit; and the thing went into liquidation.

What the receivers found is the line that gets quoted in every account, including this one, because the size of it is the whole story: a discrepancy of roughly half a million pounds between the assets the firm had claimed and the assets it actually held. The real assets were worth less than half the gap. The collateral against which the whole structure had borrowed had never existed in the quantity stated.

A single firm collapsing is a private tragedy. The Pattison collapse was a public one because of how wired-in they were. They owed money to distilleries, to grain producers, to bankers, to small suppliers across the trade, and a great many of those counterparties had extended credit on the strength of the Pattison name and the Pattison numbers. When the firm went, roughly ten other companies went down with it directly, and an uncounted tail of small suppliers and tradesmen behind them. This is the part that earns the word systemic. The Pattisons were not the largest blender in Scotland, but they were a densely connected node, and the failure did not stay local. It propagated along every line of credit that touched them.

In 1901 the brothers were tried for fraud and embezzlement. Robert, the elder and the dominant of the two, was sentenced to eighteen months; Walter to nine, served in Perth. They went to prison, served their time, and effectively vanished from the trade. The parrots, presumably, kept talking for a while in pubs that no longer had any idea what they were advertising.

The whisky loch, and the discipline that came after

The damage did not end with the creditors, and this is where the Pattisons stop being a fraud story and become an industry story.

The late-Victorian boom had not only inflated the Pattisons; it had inflated the whole trade’s idea of future demand. Distilleries had expanded, new ones had been built, and millions of gallons of spirit had been laid down in warehouses against a thirst that everyone assumed would keep growing. The Pattison crash was the pin. Confidence broke, the speculative demand evaporated, and the industry was left holding an enormous overhang of maturing stock it could not sell: what the trade came, ruefully, to call the whisky loch. A lake of whisky and no one to drink it.

That overhang took decades to drain. Distilleries fell silent through the 1900s and 1910s; many never reopened. The consolidation that followed, much of it under the Distillers Company Limited, was partly the trade reorganising itself around the wreckage so that no single over-leveraged blender could ever again pull the whole structure down. You can draw a fairly straight line from December 1898 to the cautious, inventory-disciplined, vertically careful Scotch industry of the early twentieth century. The firms that survived and grew through that long hangover were, not coincidentally, the careful ones: the William Grants quietly building Glenfiddich by hand with second-hand stills, the Cardhu of Elizabeth Cumming selling honest malt into honest blends, the houses whose entire commercial religion, as with Alexander Walker’s doctrine that the blend must taste the same forever (in Japanese), was that the thing in the bottle had to actually be the thing on the label. The Pattisons were the negative example those reputations were measured against.

The name that survives as a warning

There is no Pattisons whisky on a shelf today. The name became, for a generation in the trade, a synonym for ruin (the thing you did not want to be compared to), and then it faded even from that, into a footnote and a parrot anecdote. Robert and Walter built the most visible whisky company in Scotland and left nothing you can pour. The closest thing to a monument is structural: the reflex of caution the industry built into itself afterward, the suspicion of the blend that is too cheap to be what it claims, the long institutional memory that over-production and a single over-leveraged node are how an entire sector dies. Every careful inventory ledger and honest age statement in the century that followed is, in a small way, scar tissue from their fall.

I find it a quietly bleak kind of immortality. Most of the people I write about live on in something you can taste: a still shape, a cut point, a cask choice that is still being honoured. The Pattisons live on only in the things the industry decided never to do again. They were not stupid and they were not, at the start, dishonest; they were two dairymen who read a real opportunity correctly, scaled it on borrowed conviction, and could not tell the difference between a company that was growing and a company that was merely getting louder. The parrots could not tell the difference either. That was always the point of the parrots.

Related reading on the careful builders the Pattisons are the counter-example to: William Grant and the second-hand stills that built Glenfiddich in 1886; Elizabeth Cumming and the Cardhu she ran straight into the Walker blend; and John Haig at Cameronbridge, the grain-whisky technology that made the whole blending boom, Pattisons included, possible. For another story of bankruptcy and reinvention from the other side of the ledger, Joseph Hobbs at Ben Nevis is the outsider who failed, came back, and built something that lasted. My broader writing on whisky and who owns what is at kenimoto.dev.